Home Insurance Jumped 46% Since 2021 — Here's How to Check Your Rate

It's not just you. Home insurance has outrun inflation by 3 to 1 since 2021. Here's the data behind the spike — and the two-minute move to see if you're overpaying.

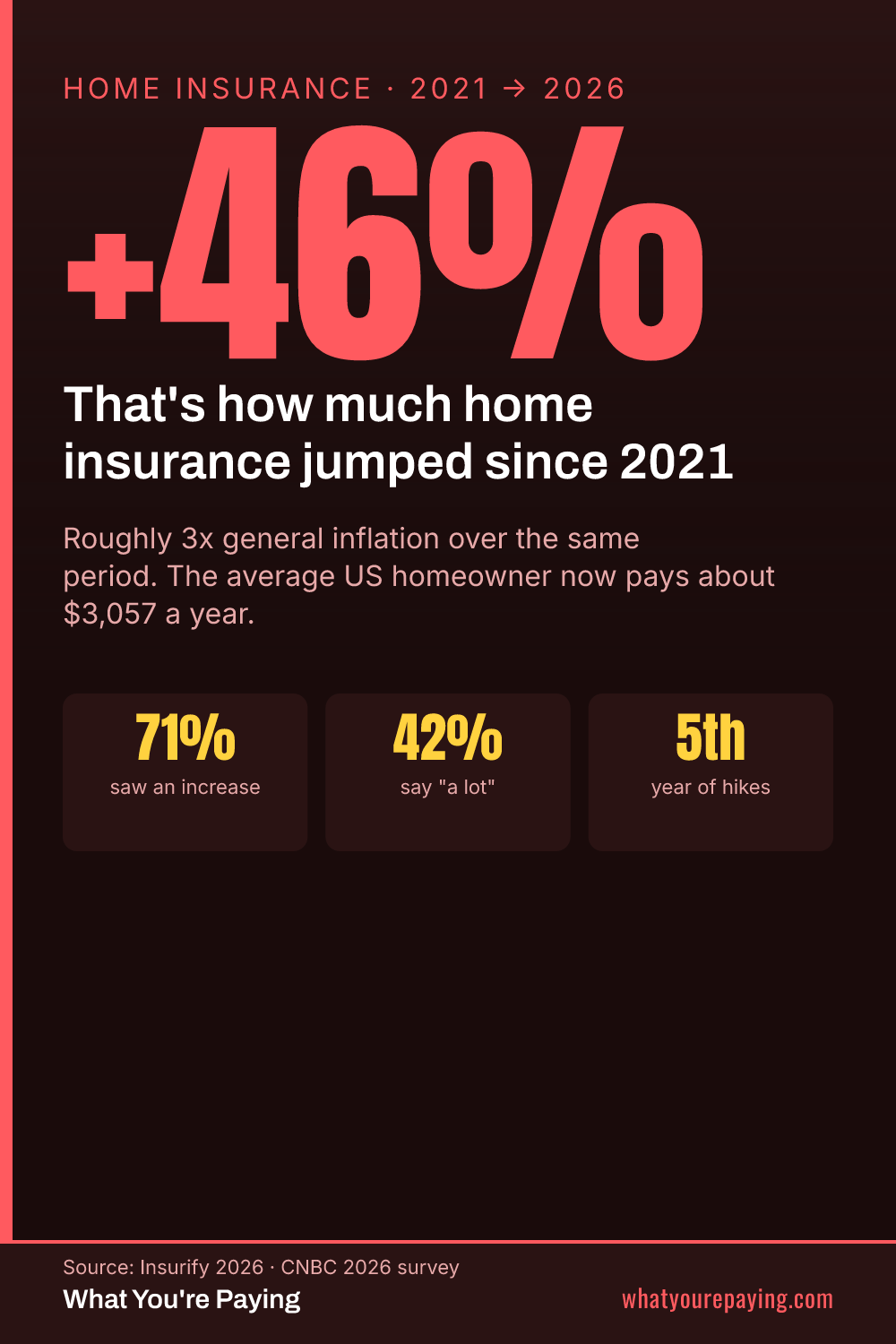

If it feels like your home insurance has spiraled out of control, the data backs you up. Insurify reports that premiums have climbed roughly 46% since 2021 — about three times the pace of general inflation over the same stretch — pushing the average homeowner's bill to around $3,057 a year.

This isn't a one-time spike. A 2026 CNBC survey found 71% of homeowners saw their premium rise, with 42% saying it went up 'a lot.' For many households, 2026 is the fifth straight year of increases. The drivers are higher rebuilding costs, more frequent severe weather, and surging reinsurance prices — none of which are in your control.

📩 Get the free 2026 Home Insurance Rate Report

The full breakdown of what's driving the spike and the discounts most homeowners miss. Free, no obligation.

What is in your control: who you buy from. Insurers raise rates on existing customers far faster than they quote new ones, so the longer you've stayed put, the more likely you're overpaying. Re-shopping, raising your deductible, and bundling home with auto are the three fastest levers.

You won't know your number until you check it. Comparing quotes is free, takes about two minutes, and doesn't change or cancel your current policy — it just tells you whether you're leaving money on the table.

Compare Home Insurance Rates — Free, 2 Minutes →Common questions

Why has home insurance gone up so fast?

Higher rebuilding/labor costs, more severe weather, and rising reinsurance costs pushed premiums up ~46% since 2021 (Insurify) — far faster than inflation.

Is this going to keep happening?

Increases are expected to continue but slow in 2026 (~4% projected). That makes now a sensible time to re-shop before the next renewal.

How do I actually lower my bill?

Re-shop your policy, raise your deductible, bundle home and auto, and claim every discount you qualify for. Comparing quotes is free.

Sources

- Insurify 2026 — Average cost of homeowners insurance

- CNBC 2026 — "42% of homeowners say insurance costs have gone up a lot"