The 8 Most Expensive States for Home Insurance in 2026

Home insurance premiums have jumped 46% since 2021. In these eight states, homeowners are getting hit the hardest — see where your state lands and how to check your rate.

Homeowners insurance used to be the boring line item on your mortgage statement. Not anymore. Premiums have climbed about 46% since 2021 (Insurify) — roughly three times the rate of general inflation over the same period — and in a handful of states the numbers have gone from annoying to genuinely painful.

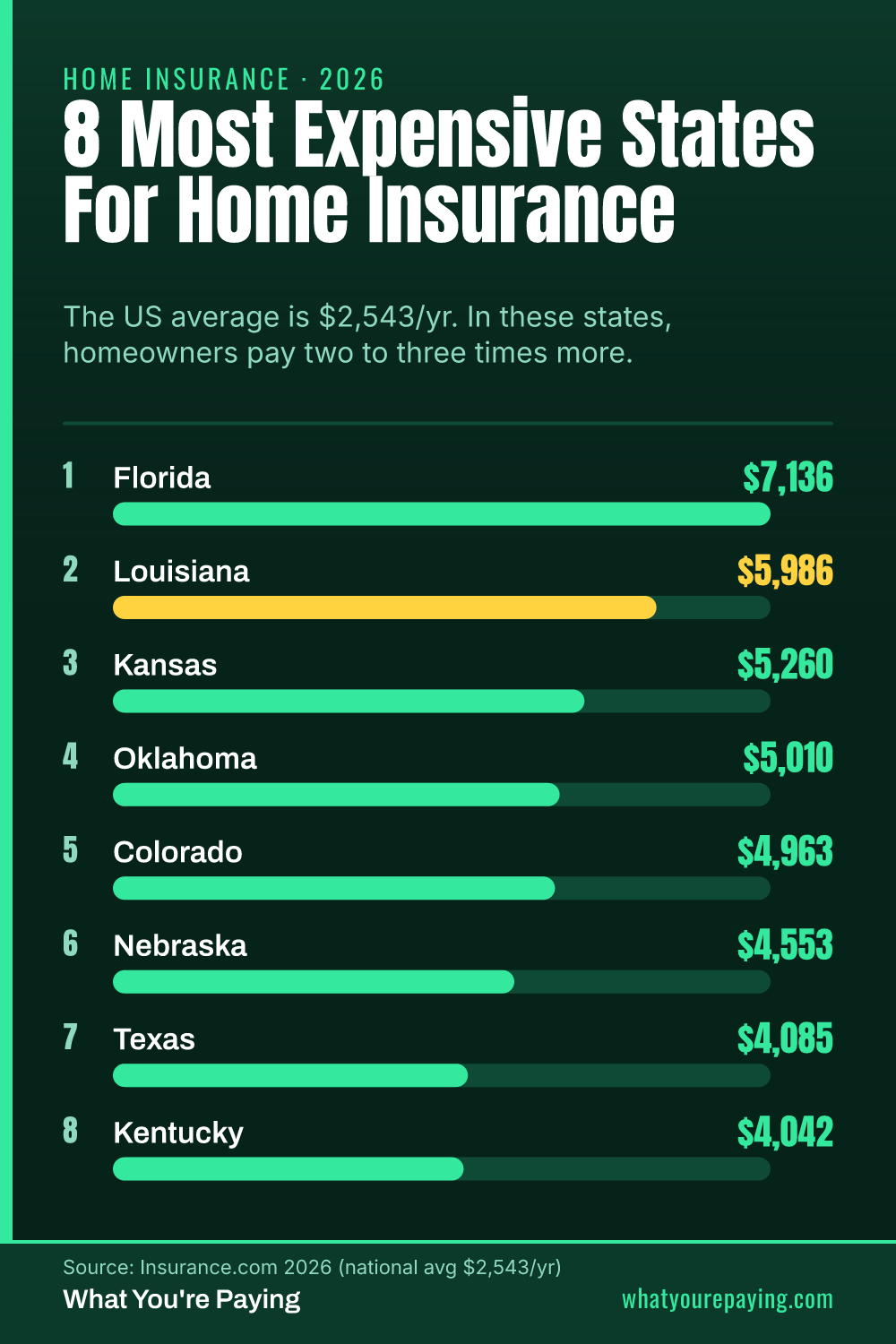

Per Insurance.com's 2026 data, the national average sits around $2,543 a year. Florida shatters it at $7,136 — nearly triple the national figure — followed by Louisiana at $5,986. The pattern is weather: every state in the top tier sits in hurricane, tornado, or wildfire country, and insurers price that risk straight into your premium.

📩 Get the free 2026 Home Insurance Rate Report (all 50 states)

The full state-by-state average premium, plus the discounts most homeowners miss. Free, no obligation.

What makes this worse is that increases stack. A CNBC survey in 2026 found 71% of homeowners saw their premium rise, and 42% said it went up 'a lot.' 2026 marks the fifth straight year of hikes for many. If you've simply auto-renewed each year, you may be paying hundreds more than you need to.

You can't change the weather, but you can change what you pay for the same coverage. Re-shopping home insurance — and bundling it with auto — is the fastest way to claw back some of that 46%. It's free to compare, and it doesn't touch your current policy unless you decide to switch.

Compare Home Insurance Rates — Free, 2 Minutes →Common questions

Why did my home insurance go up so much?

Premiums rose ~46% since 2021 (Insurify) due to higher rebuilding costs, more severe weather, and rising reinsurance costs. In high-risk states the jump is even steeper.

Can I actually lower it?

Often yes — by re-shopping, raising your deductible, bundling home and auto, and claiming discounts you may not know about. Comparing quotes is free and takes a couple of minutes.

Will comparing affect my current policy?

No. Getting quotes does not change or cancel anything. You stay put unless a better rate is worth switching for.

Sources

- Insurance.com 2026 — Most and least expensive states for homeowners insurance

- Insurify 2026 — Average cost of homeowners insurance

- CNBC 2026 — Homeowners insurance survey